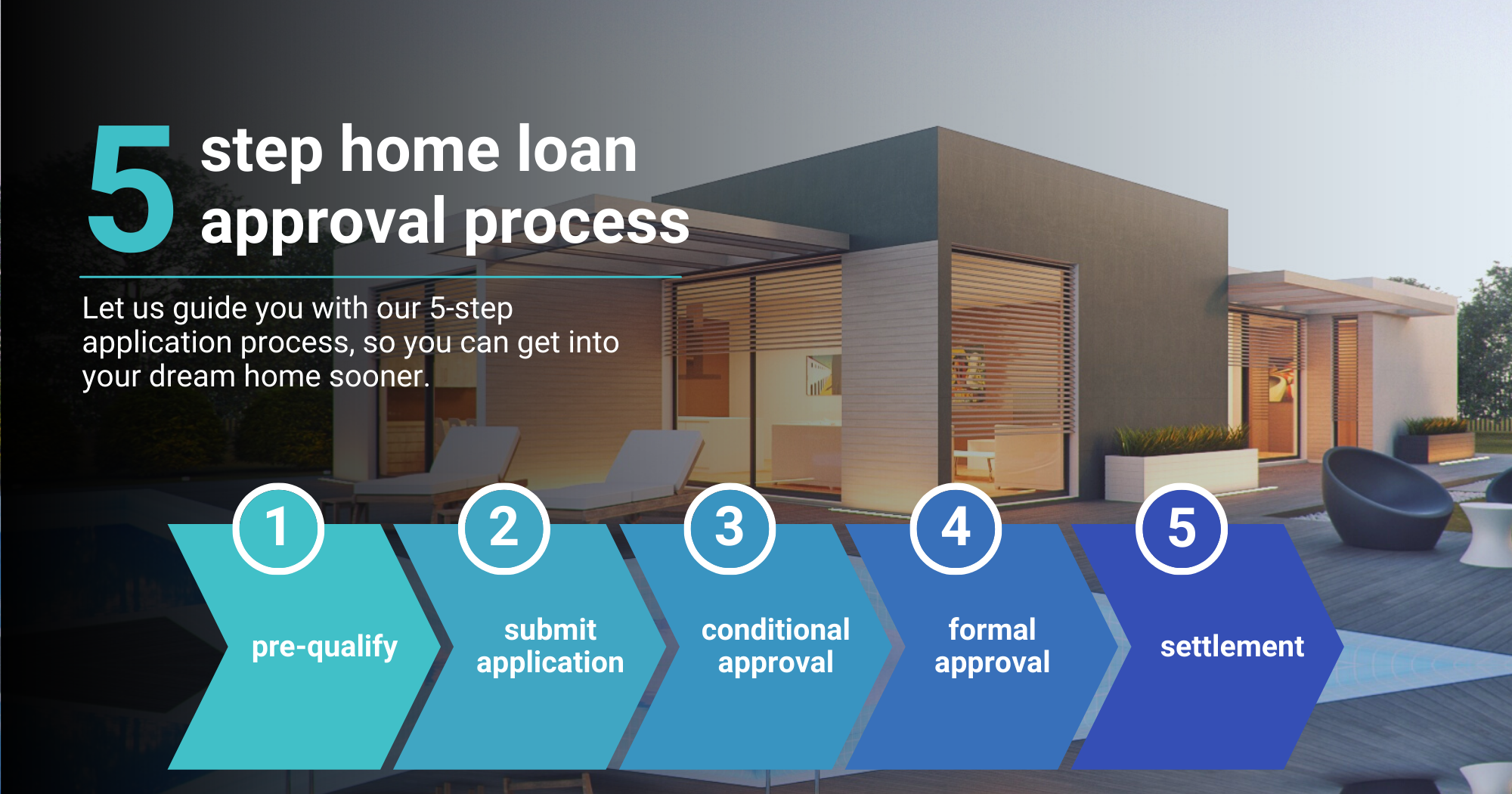

5-step home loan approval process

Investment in the share market has become high risk. It is in this type of economic climate that the Australian residential property market has historically performed well.

Buying a home is exciting but many people find applying for a home loan a bit overwhelming. If you’ve never applied for a mortgage, or it’s been quite some time since you secured your current one, then you might feel a little out of your depth.

At emoney, we’ve designed our 5-step home loan approval process to help borrowers go from pre-application through to settlement as quickly and efficiently as possible. Here’s how we do it.

1. Pre-qualify

The first thing you need to know before you start looking for a new home, is how much you can spend. There’s no point looking at million dollar houses if you can only afford half of that!

That’s why the first step in our home loan approval process is to apply for a no-obligation pre-qualification. Simply enter some basic details into our pre-qualify form and get an immediate estimate of how much you may be able to borrow.

It’s important to note prequalifying for a loan is not the same as approval. This figure is based on the information you submit. Credit checks and property valuations still need to be performed before you are granted formal approval.

The next step is to talk to a Lending Specialist about submitting an application.

2. Application

You can submit your mortgage application before or after you have made an offer on your new home. Applications received without a signed contract of sale can advance to the conditional approval stage, but formal approval will not be granted until the contract of sale has been provided and all conditions have been met.

Application forms must be submitted along with documentation to verify your identity, your income, expenses, assets and liabilities. Your lending specialist will let you know exactly which documents we require, but typically they include:

Evidence of income

- PAYG: Recent payslips & your tax assessment notices for the last 2 years.

- Self-Employed: Evidence of your own income as well as those for your business.

Details of assets & liabilities

- We require details of your assets and liabilities as well as information about your living expenses. Again your lending specialist will be able to let you know which documents to submit

Identification documents and signed contract of sale

Once we have received your application and all relevant documentation, we will run loan serviceability and credit checks to help determine whether you can comfortably afford to make repayments on the amount you’ve applied for.

3. Conditional approval

At this stage, if you submitted your application before finding a property, you now have 90 days to find your new home before the conditional approval runs out and you have to apply again. Note, conditional approval is not guaranteed approval—it is conditional on the purchase property passing assessment.

If you have already provided us with the signed property contract, we will order a formal valuation on the property. The valuation takes place onsite to assess whether the property is suitable for mortgage purposes. We will be provided with a report outlining the property’s value and any associated risk factors. The final valuation will be based on comparable sales in the area and the condition of the property.

If you have applied to borrow more than 80% of the property’s value, you will be required to pay a lender’s mortgage insurance (LMI) premium. Your application must be approved for LMI before it can move to formal approval.

4. Formal approval

Once all conditions have been met, your home loan will go unconditional and a formal approval will be issued. If you have a finance clause in the sale contract, formal approval means you are now committed to purchase the property.

We will send the loan contract documents to your solicitor or conveyancer which you should sign and return to us as soon as possible. The quicker you review and sign the loan documents, the sooner your loan will settle. Once we receive your signed loan documentation, your settlement date can be arranged.

5. Settlement

emoney will make the final settlement payments to the property’s vendor and you will be notified once this has taken place. At this point you can arrange a suitable time with the real estate agent to pick up the keys to your new home.

Our lending specialists are on hand to guide you through this process and can answer any questions you may have along the way. Give us a call on 13 SAVE today.

We recommend you seek independent financial advice prior to making any decisions that could affect your financial security.

First Home Buyer's Guide

Enter your email address for instant access to our handy First Home Buyer's ebook.

Construction Loan Guide

Building a new home. Find out about the construction loan process.